If you have ever tried to track down a payment from a client who has suddenly decided that "ghosting" isn't just for dating apps, you know how frustrating the recovery process can be. When that client happens to move across the provincial border, say, from the bustling streets of Vancouver to the windy plains of Calgary, the complexity of debt recovery hits a whole new level.

At ICON Collection Solutions Inc., we often hear from business owners who are terrified that once a debt hits the two-year mark, it simply vanishes into the thin mountain air. While there is some truth to the "two-year rule," the reality is much more nuanced. Whether you are dealing with a collection agency in bc or looking for Calgary collections expertise, understanding the Statute of Limitations is the difference between recovering your $50,000 invoice and writing it off as a very expensive "learning experience."

The Golden Rule: The Two-Year Clock

In both British Columbia and Alberta, the magic number is two. According to the Limitation Act in BC and the Limitations Act in Alberta, a creditor generally has two years to initiate legal action to recover a debt.

The clock starts ticking from the date the debt was incurred or the date of the last payment. This is known as the "basic limitation period." If you don't file a statement of claim within this window, you lose the legal right to sue the debtor. (And yes, "I was on vacation for two years" is not a valid legal excuse for missing the deadline).

The "Restart" Button: Acknowledgment and Payments

Here is where things get interesting, and where many debtors accidentally trip themselves up. The two-year clock is not set in stone. It can be "reset" or "tolled" if the debtor does one of two things:

- Makes a payment: Even a payment of $5.00 can restart the entire two-year clock from the date of that payment.

- Acknowledges the debt in writing: This doesn't have to be a formal legal document. A simple email or text message saying, "I know I owe you that $10,000, I just need more time," is often enough to reset the limitation period.

We’ve seen cases where a business was just days away from being "safe" under the statute of limitations, only to send an email asking for a discount. Boom, the clock resets, and our team at ICON can get back to work. If you're struggling to keep track of these timelines, you might want to check out our 3 simple ways to better manage accounts receivables.

BC vs. Alberta: The Regional Nuances

While the two-year basic limit is the same, the way these provinces handle the "vibe" of collections can differ.

The British Columbia Landscape

Working with a collection agency in bc requires a deep understanding of the Business Practices and Consumer Protection Act. BC is quite strict about how and when a collector can contact a debtor. For instance, if you are pursuing a debt in Surrey or Vancouver, you need to ensure every step is documented to avoid "statute-barred" claims.

In BC, some debts are actually exempt from the two-year rule. Debts owed to the government (like provincial taxes), student loans, and child support arrears often have much longer, or even infinite, limitation periods. If you're looking for localized help, our collection agency in Surrey BC page offers more specific insights.

The Alberta (Calgary) Perspective

Alberta has recently stepped up its game. In 2025, the province implemented enhanced consumer protection rules. These rules are designed to prevent misleading tactics, especially in digital communications. For businesses involved in Calgary collections, this means your documentation needs to be tighter than ever.

Alberta also has an "ultimate limitation period" of 10 years. This means that regardless of when a debt was discovered, no legal action can be brought after 10 years from the date the claim arose. While two years is the standard for starting a lawsuit, the 10-year mark is the absolute "drop-dead" date for almost everything else. If you are looking for the best collection agency in Alberta, you need a partner who understands these legislative shifts.

The Wall of Excuses: A Collector's Comedy Hour

In our years of recovery, we have heard it all. When a debt is nearing that two-year mark, debtors get... creative. Here are some of our favorite (and totally real) excuses for why the check isn't in the mail:

- "My dog didn't just eat my homework; he ate my entire accounts payable folder, and I don't know who I owe money to anymore."

- "I thought the debt expired when the store changed its logo. New branding, new me, right?"

- "I’m currently living in a spiritual retreat where money isn't recognized as a valid concept. Please call back in 2029."

- "I sent the e-transfer, but I think the Wi-Fi signals got lost over the Rockies. It's probably floating somewhere near Banff."

While these make for great office stories, they don't hold up in court. A professional agency knows how to see through the "spiritual retreat" and get back to the facts of the invoice.

Why You Shouldn't Wait Until the 23rd Month

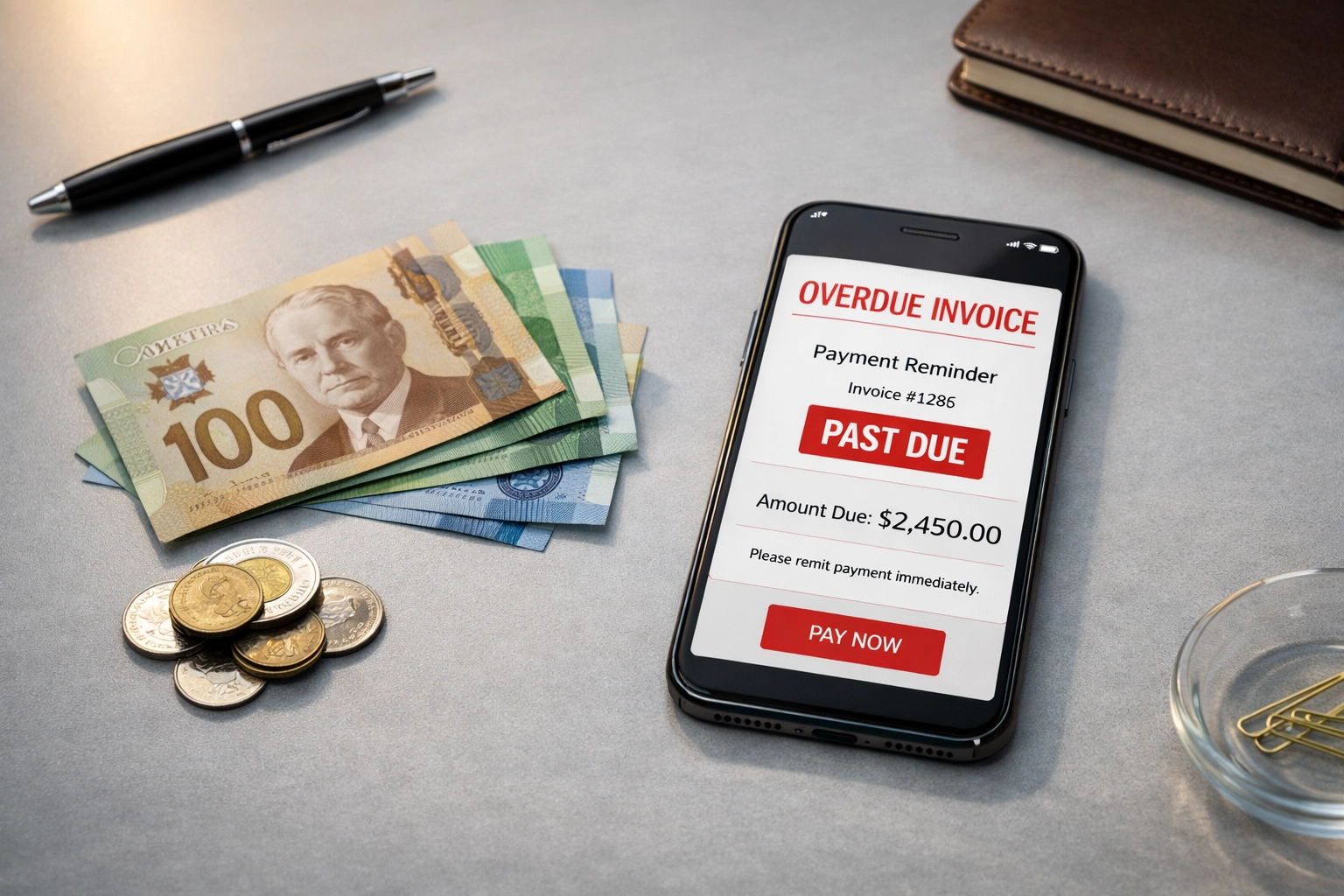

A common mistake businesses make is waiting until the very last minute to seek help. They think, "I'll give them one more chance," or "We've been friends for years." By the time they contact a professional, the debt is 22 months old, and the debtor has vanished.

Recovering a debt that is 60 days overdue has a success rate of about 85%. Once that debt hits the one-year mark, the success rate drops significantly. By the time it hits two years, you are fighting an uphill battle against the Statute of Limitations.

We recently helped a business recover $50,000 in outstanding invoices by acting quickly before the limitation period became an issue. Speed is your best friend in the recovery world.

Federal Exceptions: The "Big Brother" Factor

It is important to note that federal debts do not follow the provincial two-year rule. If you owe money to the Canada Revenue Agency (CRA) or have federal student loans, they generally have a six-year limitation period. And let’s be honest, the CRA has ways of getting their money that a standard business simply doesn't (like seizing your tax returns).

How ICON Collection Solutions Inc. Can Help

Navigating the legal labyrinth of BC and Alberta debt laws shouldn't be your full-time job. You have a business to run. Whether you are dealing with commercial debts in Edmonton or retail collections in Vancouver, we bring a professional, results-oriented approach to the table.

We use advanced tools: some might even say we're experts in how AI and automation are changing debt collection: to track down debtors and ensure that the limitation clock doesn't run out on you.

Our Strategy Includes:

- Skip Tracing: Finding debtors who think they can hide by moving from Kelowna to Red Deer.

- Legal Expertise: Knowing exactly when to escalate a file to legal action before the two-year window closes.

- Effective Communication: Using best collection letter templates that actually get a response.

Don't Let the Clock Run Out

The difference between "money in the bank" and "bad debt expense" is often just a matter of timing. If you have outstanding invoices in BC or Alberta, don't wait for the two-year anniversary to celebrate.

Contact us today at ICON Collection Solutions Inc., and let’s reclaim what’s rightfully yours. Whether you need a top commercial collection agency in Edmonton or support in the heart of Vancouver, we are here to help you navigate the regional nuances and get paid.

Quick Takeaway Table: BC vs. Alberta

| Feature | British Columbia | Alberta |

|---|---|---|

| Basic Limitation Period | 2 Years | 2 Years |

| Ultimate Limitation Period | 15 Years | 10 Years |

| Clock Reset Mechanism | Payment or Written Acknowledgment | Payment or Written Acknowledgment |

| Special 2025 Protections | Standard BC Consumer Protections | Enhanced Digital Communication Rules |

| Common Exemptions | Fines, Taxes, Student Loans | Fines, Taxes, Student Loans |

This content is for informational purposes only and does not constitute legal advice.

.jpeg)

.png)

.png)

.png)

.png)

%20(1).jpg)

%20(1).jpg)

.jpg)