We’ve all been there. A new lead comes in, the numbers look fantastic, and the client seems eager to get started. It’s that "new contract smell", better than a new car, right? You’re already calculating the profit, maybe thinking about that upgrade for the office or finally taking the team out for that long-overdue steak dinner in downtown Calgary or Vancouver.

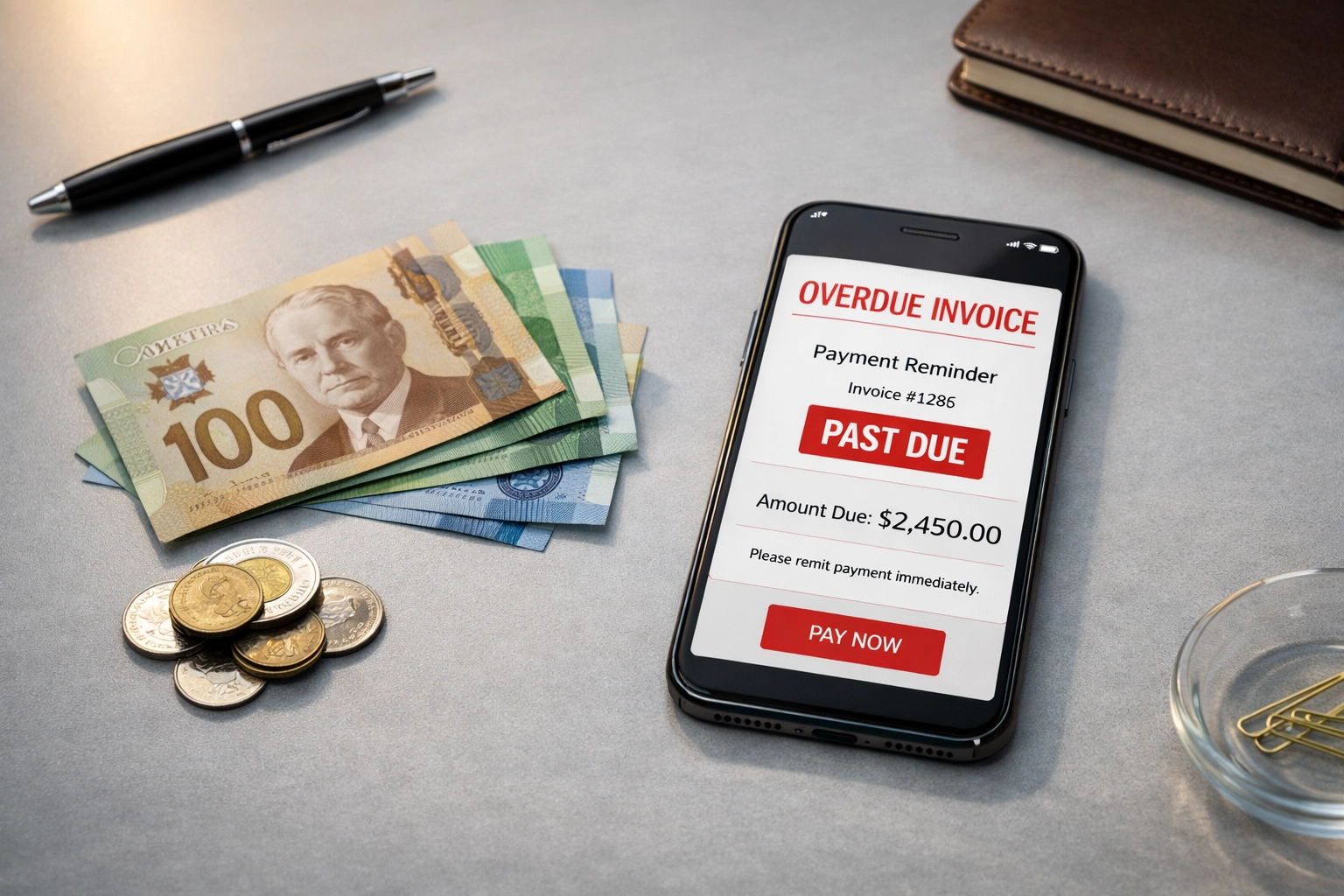

But then, 45 days later, the silence hits. The invoice is overdue. Your emails are ignored. Suddenly, that "dream client" has turned into a nightmare that is eating your cash flow alive.

At ICON Collection Solutions Inc., we see this cycle every single day. While our job is to recover what’s owed to you, we’re also huge fans of prevention. The most profitable debt is the one you never have to collect because you screened the client properly from day one. In fact, performing a simple credit check before signing on the dotted line can save your business thousands, if not tens of thousands, of dollars.

The "Honeymoon Phase" vs. Reality

When a new client walks through the door, they are on their best behavior. They’ve got the shiny pitch, the professional-looking LinkedIn profile, and a "guarantee" that they are growing fast. But excitement is not a financial strategy.

Extending credit (which is exactly what you are doing when you offer Net-30 or Net-60 terms) is essentially giving that client an interest-free loan. Would you walk into a bank in Edmonton and ask for $10,000 without them checking your credit score? Of course not. So why do so many B2B businesses hand over $10,000 worth of services or products without doing the same?

Why Credit Checks are Your Best Defense

A credit check isn’t just a "yes/no" button; it’s a window into how a company operates when the lights are off and the pressure is on. Here is why it’s a non-negotiable step in your onboarding process:

1. Risk Mitigation (The "Sleep Better" Factor)

By assessing a client’s creditworthiness and payment history, you can identify red flags before they become your problem. If a company has a history of paying their suppliers 90 days late, guess what? You aren’t going to be the "special one" they pay on time. A credit report tells you if they are financially stable or if they are "robbing Peter to pay Paul."

2. Fraud Prevention

Identity theft isn't just for individuals. We’ve seen cases where "ghost companies" are set up with stolen credentials to rack up massive B2B debts before vanishing into thin air. Incorporating anti-money laundering (AML) checks into your credit reporting helps you spot these red flags. It’s better to lose a "sale" to a fraudster than to lose $50,000 in inventory.

3. Setting Realistic Credit Limits

Not every client is a "Tier 1" client. A credit check allows you to set appropriate limits. Maybe you start a new client with a $2,000 limit and cash-on-delivery (COD) terms for the first three months. Once they prove they can play by the rules, you can extend those terms. This keeps your exposure manageable while you build trust. For more tips on this, check out our guide on 3 simple ways to better manage accounts receivables.

The Math: The True Cost of a $5,000 Unpaid Invoice

Let’s talk numbers. If a client defaults on a $5,000 invoice, you haven't just lost $5,000 in profit. You’ve lost:

- The cost of the materials or goods sold.

- The labor hours spent by your team (which you still have to pay for).

- The overhead (rent, power, software) used during that project.

- The opportunity cost (the time you could have spent on a paying client).

If your profit margin is 20%, you need to generate $25,000 in new sales just to break even on that one $5,000 loss. When you look at it that way, a $50 credit check seems like the bargain of the century.

The "Creative" Excuses We Hear in Western Canada

If you decide to skip the credit check and things go south, you’ll eventually find yourself chasing the payment. Over the years, we’ve heard it all at ICON. When businesses in Alberta and BC don’t want to pay, their creativity suddenly peaks.

Here are a few of our favorites (yes, these are real):

- The "Act of God": "A rogue beaver chewed through our fiber-optic cable, and we haven't had internet to process e-transfers for three weeks." (Classic BC excuse).

- The "Mysterious Accountant": "Our accountant, Brenda, is currently trekking through the Himalayas and she’s the only one with the physical key to the checkbook."

- The "Invisible Invoice": "I never received the invoice. Or the three reminders. Or the registered letter. Are you sure you have my email right? Oh, you sent it to info@? Yeah, I never check that."

- The "Post-Dated Pipe Dream": "The check is in the mail! I dropped it in the box in Red Deer personally. It must be a slow mail day." (It’s been 14 days, Dave. Canada Post isn't that slow).

While these are funny in hindsight, they aren't so funny when your payroll is due on Friday. Screening prevents you from ever having to hear Brenda's Himalayan adventures.

Navigating the Landscape in BC and Alberta

In Western Canada, we have specific legal frameworks that affect how you can recover money. Whether you are dealing with collections in Calgary or looking for a collection agency in Surrey, BC, the rules of the game matter.

In British Columbia, the Civil Resolution Tribunal (CRT) handles many small business disputes, but the Statute of Limitations is a ticking clock (usually two years from the date the debt was acknowledged). In Alberta, the Court of Justice is often the venue for these battles.

By running a credit check, you can see if a company is already embroiled in multiple lawsuits or has a trail of judgments against them in these provinces. If they’re already being sued by three other contractors, you don’t want to be fourth in line.

How to Build a Bulletproof Screening Process

You don't need a massive legal department to protect yourself. A simple, consistent process will do 90% of the work:

- Use a Formal Credit Application: Make every new client fill one out. It signals that you are professional and serious about your money. (Pro tip: Ask for trade references: and actually call them!)

- Pull the Report: Use services like Equifax or Dun & Bradstreet. Look for the "Paydex" score or similar metrics that show payment trends.

- Check for "Lien" Activity: See if they have any registered security interests or liens against their assets.

- Trust Your Gut (But Verify with Data): If a client is pushy about terms or gets defensive when you ask for a credit check, that is a massive red flag. 🚩

If you're unsure what to look for in a partner to help with this, take a look at our breakdown of the best collection agency in Alberta and what to look for.

When Prevention Isn't Enough

Sometimes, even with the best screening, things go wrong. A long-term client might hit a rough patch due to the economy, or a management change might lead to a sudden stop in payments.

When that happens, don’t wait six months to take action. The longer a debt sits, the harder it is to recover. Whether it's a small invoice or a case where we helped a business recover $50,000 in outstanding invoices, professional intervention sends a clear message: your work has value, and you expect to be paid for it.

Final Thoughts

Screening new clients isn’t about being "mean" or "distrustful." It’s about being a sustainable business. Every dollar you lose to a bad debtor is a dollar taken away from your employees, your growth, and your family.

Take the extra 24 hours to run the check. Ask the hard questions. And if the data says "run," then run: no matter how big the contract looks on paper. Your future self (and your bank account) will thank you.

Need help recovering an invoice that slipped through the cracks? Or want to refine your credit policy?

Contact us today and let's reclaim what's rightfully yours. Whether you're in the heart of Vancouver or the industrial zones of Edmonton, ICON Collection Solutions Inc. is your partner in professional recovery.

Visit our About Us page to learn more about how we protect Western Canadian businesses.

Disclaimer: This content is for informational purposes only and does not constitute legal advice.

.jpeg)

.png)

.png)

.png)

.png)

%20(1).jpg)

%20(1).jpg)

.jpg)